Medicare is the infamous health insurance for Americans aged 65 and older. Everyone seems to love Medicare for its low cost, great coverage, and near-universal acceptance. For those newly eligible beneficiaries who have turned 65, Medicare can be complex and confusing. Not to mention the nuances of Medigap, Medicare Advantage, donut holes and the seemingly never ending alphabet associated with Medicare plans. Today we are going to cover the basics, or Medicare A, B, C and D.

Jump ahead to a section:

- An overview of Medicare Part A

- Medicare Part A costs in 2021

- Medicare Part B: A rundown

- Medicare Part B costs and IRMAA

- Medicare Advantage (Medicare Part C)

- Medicare Part D: Can you believe you have to pay extra?

Just as a disclaimer – health insurance is confusing and Medicare is no exception. Sadly, Medicare has nuances and many new enrollees are frustrated when they realize not every medical expense is 100% covered by Medicare. Below I will walk through each letter of Medicare, what it covers, and how much it costs.

It’s important to know that each letter of the plan (Medicare A, B, C and D) has different premium, deductible and coinsurance amounts.

If you are new to Medicare and curious about Medicare Advantage, check out my book on Amazon. I give an overview of Medicare Advantage, show you how to identify a good plan, and explain the key changes in 2022. Medicare Advantage is great because it encompasses Medicare A, B, C and D.

Medicare Part A

Broadly, Medicare Part A covers hospital, skilled nursing facility and hospice services. Typically when admitted to the hospital you receive two (or more) bills. A professional bill that covers physician services (i.e. cardiologist, radiologist) and a hospital bill that covers hospital services (i.e. room and board, food, laboratory and other diagnostic tests). Medicare Part A covers the hospital portion whereas Part B covers physician services (spoiler alert!).

Medicare Part A costs in 2021

Part A has a deductible, or amount you must pay out of pocket before Medicare kicks in for inpatient coverage. This amount is $1,484 payable to the hospital. After meeting this amount, Medicare covers 100% of the hospital-based costs for days 0-60 of an inpatient hospitalization.

Beyond day 60 (heaven forbid), Medicare requires a $352-per-day coinsurance fee until day 90. Once you hit day 90, the days are considered “lifetime reserve days” which cost $704 per day. Hopefully you never need to get into this tier of hospitalization.

On the other hand, skilled nursing facilities cost $0 of coinsurance for the first 20 days, then $185.50 per day in 2021. The skilled nursing facility admission has to follow an inpatient admission of at least three days. Medicare covers hospice care at 100% by unless there is an outpatient prescription, which requires a co-pay of $5. Below is a chart that summarizes this information for Medicare Part A.

| Medicare Part A category | Cost |

| Inpatient Hospital Deductible | $1,484 |

| Daily coinsurance for days 61-90 of hospital stay | $352 |

| Daily coinsurance for lifetime reserve days | $704 |

| Skilled Nursing Facility coinsurance (after 20 days) | $186 |

| Hospice coinsurance | $0 |

Wait, what about Medicare Part A premiums?

Remember how annoying it was to pay the FICA tax each paycheck? Well if you or your spouse did that for 40 or more quarters, Medicare Part A comes at no cost. For those who worked less than 40 quarters, an adjusted premium is added on each month to maintain eligibility.

Medicare Part B in 2021

As I mentioned before, Medicare Part B covers physician services and more not covered by Medicare Part A. Part B coverage begins when the Part B deductible is met, which is $203 in 2021.

After the Part B deductible is met, Medicare covers 80% of the approved service expenses and the patient responsibility will be 20%. For preventive services such as mammograms, osteoporosis or other screenings, Medicare usually covers 100%.

Part B covers all outpatient physician fees and diagnostic procedures such as bloodwork and imaging. It can also cover treatments like transfusions, dialysis, chemotherapy and some outpatient procedures.

When thinking about Part B, it is easy to think about everything done outside of the hospital (although it does cover some things performed at a hospital). Durable Medical Equipment is also covered by Part B if approved by Medicare for your specific needs.

Medicare Part B Costs in 2021

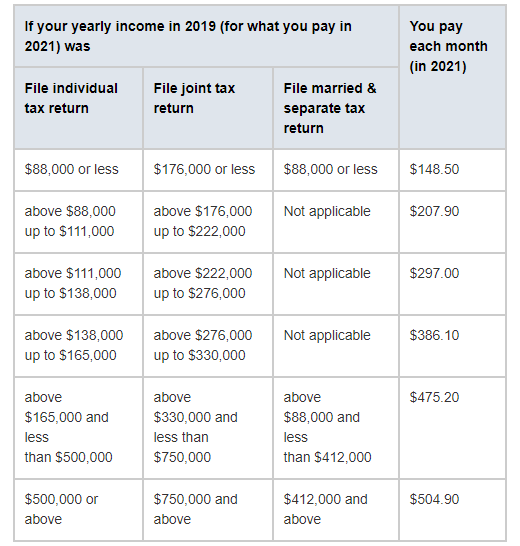

Part B does have a monthly premium, which in 2021 amounts to $148.50. If you purchase a Medicare Advantage plan, the premium is in addition to the base Part B premium. The Part B premium is income-adjusted based on what you made two years prior to the plan year. So for 2021, the premium depends on how much income you earned in 2019. This is called the income-related monthly adjustment amount or IRMAA. The adjustment table is as follows:

The difficulty with Medicare Part B is that for treatment that you receive, you really don’t have a great idea of what you will pay. Seemingly, 20% of the Medicare approved rate is great – but you don’t know what amount the 20% will be. There is a lot of guesswork for what you will pay since you aren’t quite sure what was charged. Sadly, this can lead to some surprise bills. 20% of a very expensive procedure can amount to thousands of dollars that you will be left to pay.

In situations like this, I find Medicare Advantage to be a good investment. You typically have a fixed co-pay for physician visits and an out-of-pocket max on the plan in total. This way you can insulate yourselves from surprise costs by limiting the amount you are responsible to pay. Again, Advantage plans cover Medicare A, B, C and D.

Medicare Part C (AKA Medicare Advantage)

Medicare Part C is also known as Medicare Advantage. Advantage plans have to at least include Medicare Part A and Part B, but typically add on Part D and other broader coverages. Additionally, Part C has recognizable sponsors such as Humana, UnitedHealthcare, and Aetna.

Many of the Medicare Advantage plans include A, B, and D coverage all wrapped up into one monthly premium, yearly deductible and out-of-pocket max. They also include fun extras like vision, dental, transportation and more.

Next, Medicare Advantage plans are great for beneficiaries that are familiar with employer-sponsored health insurance because they look and feel the same. Many Medicare Advantage plans are Health Maintenance Organization (HMO) plans and are $0 on top of your normal Part B premiums.

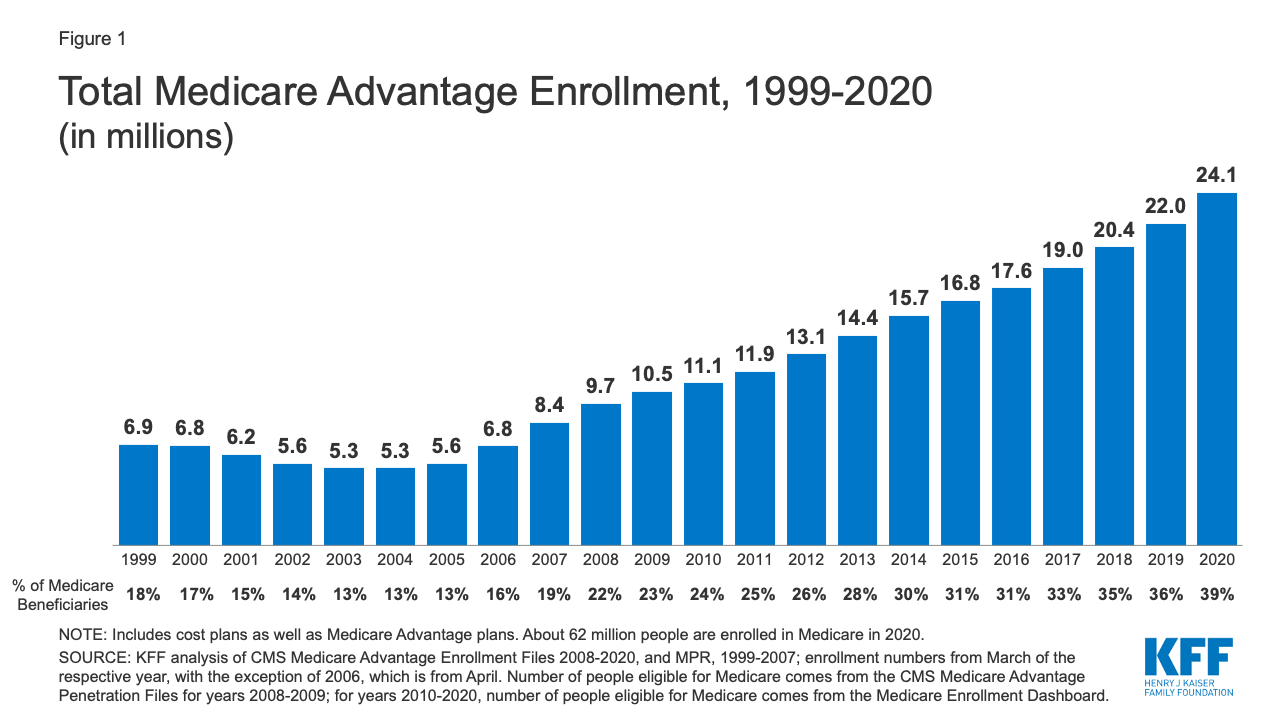

Part C Growth

Part C or Medicare Advantage enrollment has been increasing quite a bit over the past 10 years. The below graph from the Kaiser Family Foundation highlights the adoption of these plans. As you can see, nearly 40% of all Medicare beneficiaries have a Medicare Advantage Plan. I expect this number to grow as the baby boomer generation continues to become eligible for these benefits.

With the increased enrollment, I see many Medicare Advantage plans becoming more competitive on the benefits offered – exciting stuff to come! The beautiful graphic below comes from the Kaiser Family Foundation.

Medicare Part D

Medicare Part D is prescription drug coverage. If you are eligible for Parts A and B, you can purchase a prescription drug plan or have drug coverage through your Part C Medicare Advantage plan. The types of drugs you require dictate your eligibility for certain prescription drug coverage plans. There exist many Part D drug plans offered by big insurance companies that you would recognize like Aetna, Humana and Cigna. These have historically been relatively low cost on top of your part D premium. As these are variable by medication type, I won’t spend too much time digging into the details of these plans.

The Skinny on Drug Plans

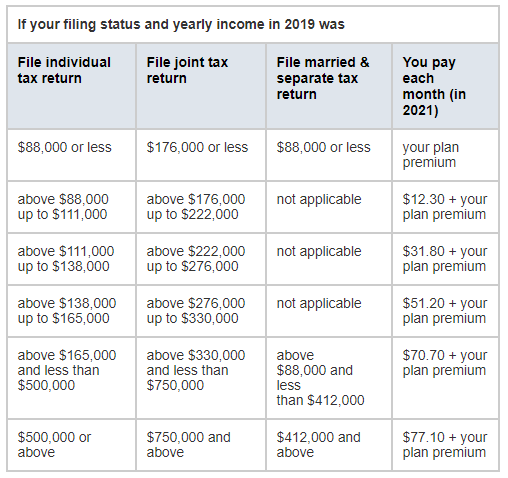

Like Medicare Part B, Part D has income adjustments commonly known by the abbreviation IRMAA.The Medicare tables are very similar to Part B and look like this:

As with Part B, these are dictated by prior year income amounts. Everyone’s situations are different, but to me it makes the most sense to keep track of all of the different parts in a Medicare Advantage plan. Keeping up with all of the individual deductibles and premiums is tough work for those without Medicare Advantage, but more power to you if that’s what you elect to do.

The Final Word

I hope you all now know Medicare A, B, C and D. If you need help or clarity provided to you, contact me to learn more.

Comments

8 responses to “Medicare A, B, C and D: An overview (2022 Update)”

[…] Previous Understand the basics of Medicare: Easy as A, B, C (and D) […]

[…] Understand the basics of Medicare: A, B, C and D […]

[…] Advantage and Medigap are both related to Medicare, but are each mistaken for the other. Here I will provide a quick overview of each and help clarify […]

[…] 20/80 coinsurance is the standard amount for traditional Medicare part B. […]

[…] or Medicare Supplemental Insurance, is a plan that can be purchased in addition to Medicare Parts A and B. These plans help cover out of pocket costs and are less restrictive than Medicare Advantage […]

[…] Medigap is a supplemental health insurance plan that offsets the costs of Medicare. For those with Medicare Part A and Part B, Medigap can be purchased for an additional premium. The plans typically help cover the cost of […]

[…] Medicare A, B, C and D: An overview […]

[…] Medicare A, B, C and D: An overview […]