Medicare Advantage and Medigap are both related to Medicare, but are each mistaken for the other. Here I will provide a quick overview of each and help clarify which one is better for your specific needs.

If you are considering Medicare Advantage, check out my book on Amazon.

Medigap

Medicare Supplemental Insurance, also known as Medigap, is a plan sold by private insurance companies. These supplemental plans help cover some of the costs associated with traditional Medicare, like copayments, coinsurance and deductibles. While Medicare is relatively comprehensive as a health insurance, out-of-pocket expenses can still add up.

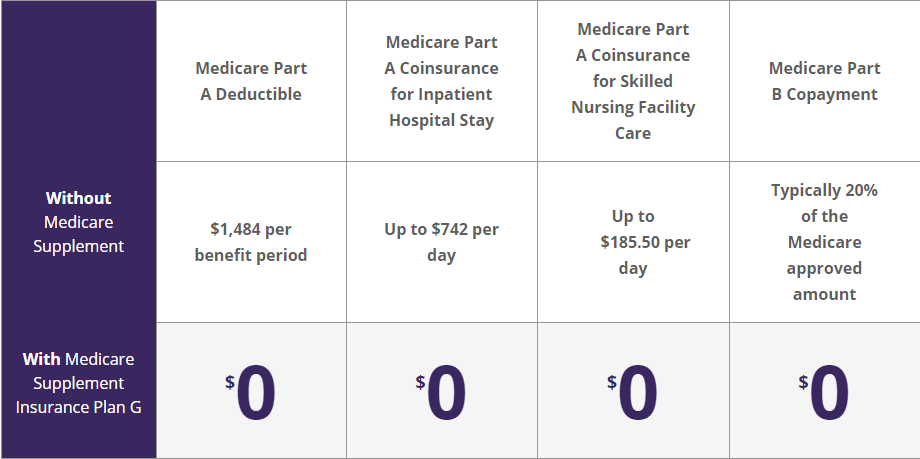

Different plans impact different expenses not fully covered by Medicare. Some of the plans impact the percentage of coinsurance and help lower the costs once you’ve hit your deductible. Other plans change the deductible or the amount of the copay for specific services. The image below shows a Medigap Plan G from Aetna and how it can impact costs:

As you can see, this Medigap plan is geared towards reducing Part A (hospital-based) costs associated with traditional Medicare.

There are 10 types of Medigap plans (A, B, D, G, K, L, M and N). C and F used to be plans, but are no longer available to newly eligible Medicare recipients. The letters don’t have a specific meaning, but are a way of standardizing the types of plans across private insurers.

The below graphic from Medicare’s website highlights the standardization process across the letters:

One thing to keep in mind is that each plan has a premium that is paid monthly that is IN ADDITION TO your normal part B premium, of which the base is $148.50/month in 2021 (before any income adjustments if applicable). Picking one of these plans will increase your premium each month but alter another portion of your plan. These don’t include Part D drug coverage, so you’ll have to purchase a separate plan if you want prescription drug coverage.

It is the law that you cannot have both a Medigap plan and a Medicare Advantage plan, so choose wisely.

Medicare Advantage

Medicare Advantage is similar to Medigap in that both are offered by private health insurance companies. These plans are similar to Medigap in that there is an additional premium each month on top of your part B premium.

Advantage plans distinguish themselves from Medigap plans in that they look like comprehensive private health insurance plans – similar to what you would have received from your employer. They are typically HMOs or PPOs and require you to visit in-network providers and services for care. They can often include a Part D prescription drug plan and other benefits like vision, dental, transportation, and telehealth.

My favorite part about Medicare Advantage is that the plans include an out-of-pocket max. This means that in case of unexpected or high health expenses, you will not pay more for services above a certain point. This truly gives the beneficiary a peace of mind about their health expenses.

When trying to select a Medicare Advantage plan, its important to make sure you understand basic health insurance terminology. While no or low monthly premiums sound appealing, make sure that your deductible, copays and coinsurance are reasonable.

I would be happy to help you navigate this process.

So which should I get: Medicare Advantage or Medigap?

It is tough to say which one is truly better. In most cases, I think that Medicare Advantage plans make the most sense. If you anticipate frequent hospitalizations, there are some Medigap plans that can make sense to reduce those Part A hospital costs. Medigap plans will also provide more flexibility and options in where you receive care. If you spend a portion of your year in a different location, Medigap will allow you to be seen by any provider who accepts Medicare. Medicare Advantage will restrict care options to a smaller network of local providers.

In almost every other scenario, I would recommend a Medicare Advantage Plan. At the end of the day, they come with more comprehensive coverage, look and feel like your normal employer-sponsored plan, and can provide unique benefits. The out-of-pocket max associated with these plans provide peace of mind for those wary of spending too much money on a catastrophic health event.

Need help choosing?

If you have questions about selecting a Medicare Advantage Plan or Medigap Plan, feel free to request help.

If you want to learn more about Medicare Advantage, check out my quick book on Amazon.