This is one of the questions I receive from friends and family most often. What is the difference between an HMO and a PPO health insurance plan? Which one should I pick? As with anything health insurance-related, it’s complicated and depends on your health preferences.

HMOs and PPOs are two of the most common offerings found in employer-sponsored health insurance. They are also popular within Medicare Advantage plans and dental insurance plans. Although slightly different in make-up, they follow the same principles and use the same lingo. Let’s get started.

HMOs

HMO stands for Health Maintenance Organization, which isn’t necessarily self-explanatory. HMOs are a lower cost form of insurance that only allow certain providers to be seen. The limited number of providers is because the insurance company has a contract to pay a certain amount of money per beneficiary (you). The providers receive the same amount regardless of how many services you require. They want to make sure that you stay healthy and don’t incur them many expenses. It is a great idea in theory, because they are steering you to doctors they trust.

A gatekeeper?

Another feature of HMOs is that they require you to have an in-network primary care provider that serves as a “gatekeeper”. This means that if you want to see a specialist, you need permission from your primary care provider. The primary care provider in each case wants to make sure that it is medically necessary and appropriate to see a specialist.

The gatekeeper is following a set of HMO guidelines in their contract that dictate when it is appropriate to make a referral to a specialist. This allows insurance companies to save money by paying a fixed, expected amount and allows the providers to keep any money that they save on patient expenses. Enrolling in an HMO as a provider can make sense with the right provider group and appropriate patient population.

One exception to the gatekeeper rule found in HMOs is the use of emergency services. If you require emergent care, you do not need to get your primary care provider’s permission to visit an ER (could you imagine?).

So why would I pick an HMO versus a PPO?

A great advantage of HMOs is their cost. They tend to be one of the lower cost health plans on the market and are characterized by low monthly premiums and low or no deductibles. If you are healthy and don’t want to use a lot of health services, the providers are typically aligned

PPOs

PPO stands for Preferred Provider Organization. Sounds exactly like what I just said about HMOs, right? Right – confusion is the name of the game when it comes to health insurance. PPOs are great plans, however. They are similar to HMOs in that you are generally restricted to a certain set of providers, but the provider group is much larger. Also, going outside of the provider group to receive care is less expensive.

PPOs work differently for providers and insurance companies than HMOs. Whereas HMO participants receive a fixed amount for each individual, PPOs work by offering a discounted rate to the insurance companies. Here is an analogy:

Parents (insurance company) take their kids (you) to a baseball game. The kids want to order food from the concession stand (physician groups). The concession stand wants as many kids as possible to come to their stand, so lowers their prices for families with four or more kids. This means that they are trading out higher margins with lower volume for lower margins at higher volume. This ensures that they stay busy and remain competitive in the marketplace.

PPOs are often more expensive than HMOs but provide more flexibility. Primary care providers don’t serve as gatekeepers in PPOs and you can pay a slightly higher rate to see out-of-network providers.

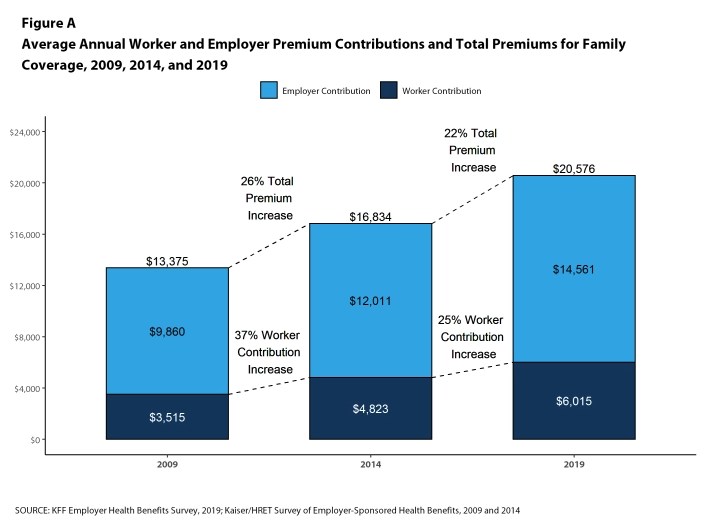

PPOs are traditionally great health plans with excellent coverage. Their downside is the monthly premium amount and the deductible. Monthly premiums, especially for families, are high under PPOs and are trending upward year over year. See below graph to visualize just how quickly insurance premiums have risen over the past ten years.

The below graphic is one from The Kaiser Family Foundation highlighting the rising costs of healthcare for employers and employees.

So which one is better, HMO or PPO?

Sadly, health insurance is not a one-size-fits-all system. If you don’t incur many health expenses and don’t care about who your doctor is, the HMO is the way to go. If you incur an average-to-high amount of health expenses and have a great relationship with your doctor, the PPO offers the broadest coverage options at a higher cost.

So which one is better for Medicare Advantage?

Again, it depends on who is asking. There are some really good HMO Medicare Advantage plans that offer many benefits, but restrict the providers you can see. If you are a senior looking for a good HMO Medicare Advantage plan, make sure to be thorough in reading through the provider, pharmacy, and prescription lists. This will help ensure your required health needs are covered and that you can find a great doctor. Most of the HMO Medicare Advantage plans I have seen are $0 additional premium each month.

PPO Medicare Advantage plans offer more flexibility in provider options but carry an additional premium amount to Medicare Part B. To learn more about Medicare Advantage, check out my book on Amazon.

What about dental HMOs and PPOs?

Dental HMOs and PPOs follow the same principles here. HMOs will have very low premiums, but a highly restricted number of available dentists. PPOs will have more options, but be higher cost on a monthly basis. I’ve chosen a PPO because I love my dentist and did not want to get forced into another dentist’s office.

I also had a horrible experience with a dentist when I had an HMO. He told me I had a cavity, but he was not going to fill it because he would not receive any additional money for doing so. If you recall, HMOs pay providers a fixed amount for providing services. This means whether or not he filled my cavity, he would get paid the same amount. Filling my cavity would have cost HIM money, so he refused to do it.

Hopefully this is not a typical scenario for HMO participants of any kind, but since that time I have selected a PPO to keep my new dentist.

HMO versus PPO

If you need help choosing between and HMO and a PPO, reach out to me for help.

Comments

2 responses to “HMO versus PPO: Learn the difference”

[…] HMO versus PPO: Learn the difference […]

[…] HMO versus PPO: Learn the difference […]