Medicare Advantage Plans or “Medicare Part C” enrollment has nearly doubled in the last decade. What exactly are these plans? Should you get a Medicare Advantage Plan? I’ll help clarify what they are and who should get them.

In this guide we will review:

- An overview of Medicare Advantage

- The difference between Medicare and Advantage plans

- The difference between Medicare Advantage and supplemental Medicare

- The costs of Medicare Advantage

- How to pick a Medicare Advantage plan

Medicare Advantage Plans in 2022

Medicare Advantage Plans give Medicare beneficiaries the option to enroll in private health plans instead of traditional Medicare. Most of these come in the form of a Health Maintenance Organization (HMO) or Preferred Provider Organization (PPO). You will likely recognize many of these plans as some of the big insurance industry names provide them. Common ones include Humana Medicare Advantage or AARP Medicare Advantage Plans from UnitedHealthcare. These plans are often low-cost plans that take the place of your traditional Medicare. They are an additional fee on top of your typical Medicare Part B premium. Even so, Medicare Advantage plans have many perks but are not always the best solution for everyone.

To learn more about Medicare Advantage, check out my book below on Amazon!

What’s the difference between Medicare and Medicare Advantage?

Medicare Advantage often provides more benefits like dental care, prescription drug coverage, vision care, telehealth and more not covered by traditional Medicare. Often, these come at an additional cost per month, but there are several Medicare Advantage plans without an additional premium. The plans generally have restrictions on which doctors you can use. They also encourage the use of “in-network” services and providers to lower the cost of care. These steer you to “high-value” providers that they trust to manage your care in a cost efficient and high quality manner. This means that you need to be very sure that all services provided to you are in-network.

On a personal note, I have had an in-network dermatologist send a laboratory sample to an out-of-network laboratory. I was unaware of this happening and had to pay a medical bill that was much higher than I expected. Many Medicare Advantage plans also require prior authorization before receiving specialty care or procedures. This means that a member from your physician’s or hospital’s team will need to reach out to the insurance company to ensure that they will pay for the procedure.

Medicare provides traditional hospital coverage (Part A) and outpatient and physician care (Part B). Also, traditional Medicare has prescription drug coverage via Part D, which is optional for an additional cost. Advantage plans generally cover each of these parts, plus more. See my breakdown of traditional Medicare here.

Medicare Part C

Medicare Advantage is known as Medicare Part C. Whereas A and B are covered under your traditional Medicare benefit, Part C must be purchased separately. I love Medicare Advantage because it covers A, B, D (often), but also comes with a ton of other benefits for minimal to no extra cost.

Is Medicare Advantage the same as Medigap?

No, Medigap helps to cover costs incurred by traditional Medicare like copays and deductibles for inpatient care. Medigap does not generally provide coverage for vision, dental, or long-term care. Medigap is an additional cost to your Medicare Part B premium.

How much does Medicare Advantage cost?

The most common Medicare Part B monthly premium cost in 2021 is $148.50. There are exceptions to this deductible depending on income, which can adjust the amount owed (see chart below for explanation). Medicare Advantage monthly premiums can vary depending on the coverage plan and region of the country. Furthermore, some monthly premiums for Medicare Advantage are $0 (in addition to the Medicare premium), while the average Medicare Advantage premium is $21 in 2021. Make sure to factor in the Medicare Part B premium into your overall monthly premium amount.

Traditional Medicare Premiums by Income for 2021

| File individual tax return in 2019 | File joint tax return in 2019 | File married & separate tax return in 2019 | You pay each month (in 2021) |

| $88,000 or less | $176,000 or less | $88,000 or less | $148.50 |

| above $88,000 up to $111,000 | above $176,000 up to $222,000 | Not applicable | $207.90 |

| above $111,000 up to $138,000 | above $222,000 up to $276,000 | Not applicable | $297.00 |

| above $138,000 up to $165,000 | above $276,000 up to $330,000 | Not applicable | $386.10 |

| above $165,000 and less than $500,000 | above $330,000 and less than $750,000 | above $88,000 and less than $412,000 | $475.20 |

| $500,000 or above | $750,000 and above | $412,000 and above | $504.90 |

What about co-pays?

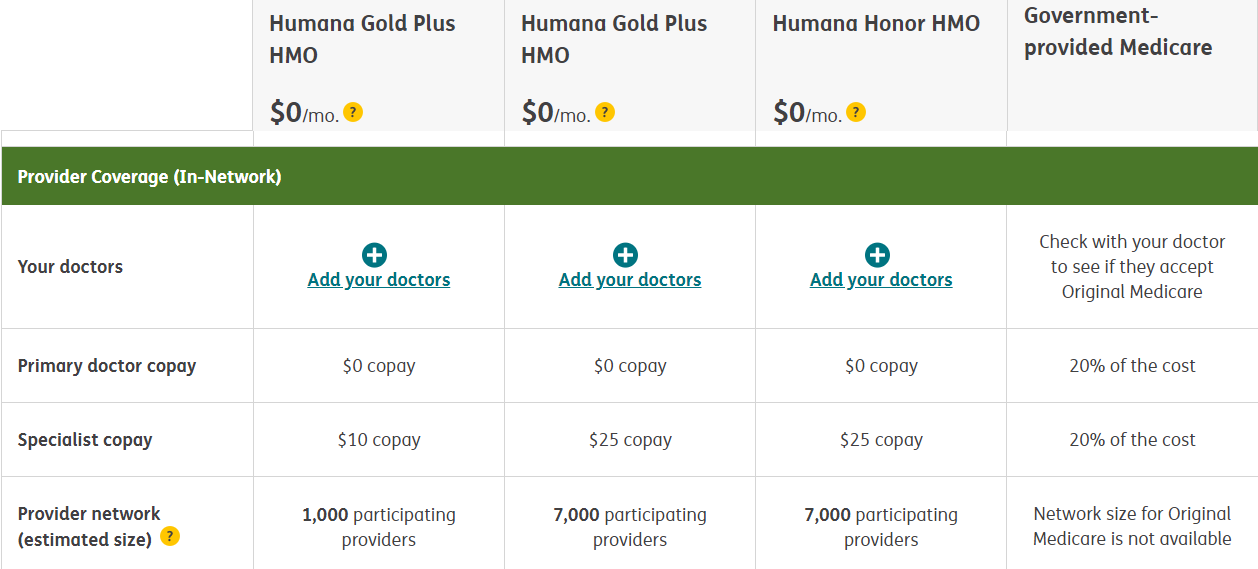

Undoubtedly, Medicare Advantage is similar to your traditional PPOs and HMOs when it comes to co-pays. Many Medicare Advantage plans have co-pays for visits to their primary care doctor or specialist (see below graphic). These co-pays vary depending on whether or not the provider is in network and whether or not they are a specialist. The co-pay is generally paid before the deductible is met. Medicare differs in that once your deductible is met for Part B, you will pay 20% of the Medicare-approved amount for each primary care or specialist visit.

Example of Humana Medicare Advantage Plan in Sumter County, Florida.

What type of Medicare Advantage plan should I get?

Medicare Advantage plans differ by zip code in both availability and price. Here is a website that can be used to find the available plans in your area. When finding a plan, scrutinize it as much as possible and make sure you understand the basic terms of health insurance. Here are a few things you should consider before picking a plan:

Affordability of Medicare Advantage

- Pick a plan that has a premium that can fit your budget easily. The Medicare Advantage premium is additional to your normal Medicare Part B premium, so keep that in mind as you factor in your monthly spend.

- Select a plan that has a deductible and out-of-pocket max that you would be comfortable spending. In short, you want to have enough in liquid savings that you can use if you incur unexpected health expenses.

- Keep in mind that Medicare premiums have risen a few dollars per year over the past few years. Costs will likely continue to rise each year, so don’t pick a plan at the top of your price point only to find it is unaffordable next year.

Coverage in Medicare Advantage plans

- Next, think about what you need out of a plan. Advantage plans often pay for things like telemedicine, dental, transportation, prescription drugs and vision. Think about purchasing a plan for your specific needs and leaving out the things you will not use.

- Take note of whether or not your doctor and pharmacy of choice are in-network with your plan. In-network providers are significantly less expensive than out-of-network providers for both PPO and HMO Medicare Advantage Plans. Do your due diligence and search through their “in-network” provider, pharmacy and prescription drug lists to make sure your services are included.

Perks and Customer Service of Medicare Advantage

- Further, some of these Medicare Advantage plans offer additional perks for seniors. One of these plans is the Humana Gold Plus HMO plan. This offers access to SilverSneakers fitness programs, advisors, and social events.

- Pick a plan with great customer service. I spoke with a senior yesterday who said he chose a Humana plan because the man on the phone, Sylvester, was the best customer service representative he has ever had. Health insurance is a tricky and confusing topic – make sure you have someone that can provide you clarity.

Considerations of your health status

- Last but not least, Medicare Advantage is great for seniors in moderate to good health. Typically they can save on costs and get additional perks. If you are a senior with several chronic health conditions, Medicare Advantage may be more expensive than traditional Medicare. The higher deductible and out-of-pocket costs associated with a Medicare Advantage plan can quickly add up if you experience an unexpected health crisis or have chronic conditions.

- On the other hand, if you frequently utilize health services, these plans have an out-of-pocket maximum. This means that after a certain amount of money spent, your insurance company will pay the remainder of the balances. Traditional Medicare Part B does not have this feature and could end up being more costly than Medicare Advantage.

Tricks to picking the best plan

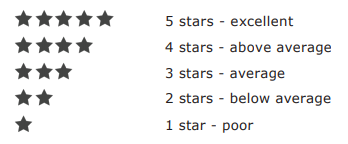

Medicare Advantage Plans, like all other insurance plans, have something called a “Summary of Benefits”. This explains the costs for each type of service covered in the plan. These sometimes include the benefits included in traditional Medicare, which are extremely important to know. Associated with the Summary of Benefits are the Provider Directory, Pharmacy Directory, and CMS Plan Ratings. The provider directory will show you all of the in-network providers with the specific plan. Pharmacy directories list all of the pharmacies that are in-network with the plan. CMS Plan Ratings are produced by the Center for Medicare and Medicaid Services (for some reason called just CMS and not CMMS). As expected, the stars represent the following rankings:

Each advantage plan will be ranked on their health plan as well as their drug plan. Make sure to check both and shoot for as close to five stars as you can get within your budget.

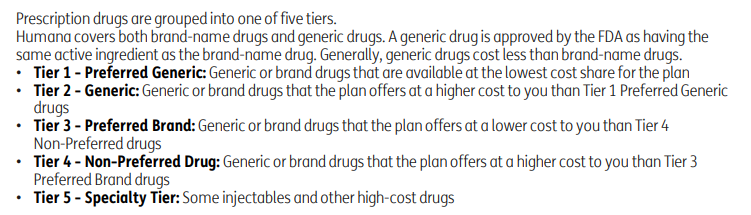

Each plan should also include a Medicare Prescription Drug List or “formulary”. This displays all of the drugs covered by their plan and assigns a tier to each. The Tiers for Humana look like this:

If you have prescriptions, make sure to enter them into the plan to see how it falls into the tiers. The lower the tier, the less expensive the drug will be for your plan.

When can I get Medicare Advantage?

You can enroll in these plans during the open enrollment period each year. The dates for open enrollment in 2020 were October 15th through December 7th. During this time, you can change from traditional Medicare to a Medicare Advantage plan and vice versa. You will also be able to switch from one Medicare Advantage plan to another.

There is a second, separate Medicare Advantage Open Enrollment Period from January 1st to March 31st in 2021. This allows someone with Medicare Advantage to switch to another Medicare Advantage plan or go back to traditional Medicare. The ability to switch plans during a three-month trial period is unique to Medicare Advantage.

The plans also have a few special enrollment periods that allow you to select a new plan under certain circumstances. One of these circumstances is if you relocate. As I mentioned earlier in this post, Medicare Advantage plans are location specific. The location is important because it determines which providers you are able to see in your network. If you move, you will no longer be in network with your local providers, so your plan will have to change.

What’s the bottom line?

Clearly, I think these plans are incredible for the right people. If you are a generally healthy senior who will take advantage of Medicare Advantage benefits, then Advantage plans are perfect for you. At a low cost on top of your traditional Medicare Part B premium, these plans can cover vision, dental, transportation, wellness, prescription drugs, and more. Another benefit of these plans is that they typically have an out-of-pocket maximum. This means you will not pay more out-of-pocket than this specified amount, a feature not found in traditional Medicare.

Conversely, the downside to these plans for the budget-conscious is the additional monthly premium associated with the plans. While most are less than $50 per month, the premium amount adds up throughout the course of a year. Another downside to these plans is the restriction on providers. If you have a primary care or specialty physician that is out-of-network you will incur extra charges if you do not switch to an in-network provider. This requires careful, diligent research on your part to stay in-network.

If you have questions about Medicare Advantage, I can help.

Comments

7 responses to “Ultimate Medicare Advantage Guide (2022 Update)”

[…] Your ultimate guide to Medicare Advantage in 2021 […]

[…] Your ultimate guide to Medicare Advantage in 2021 […]

[…] Previous Your ultimate guide to Medicare Advantage in 2021 […]

[…] Next Medicare Advantage: Your ultimate guide in 2021 […]

[…] Medicare Advantage: Your ultimate guide in 2021 […]

[…] Medicare Advantage: Your ultimate guide in 2021 […]

[…] is great for some people, but still not as comprehensive as Medicare Advantage. For example, vision, dental, long-term care and hearing aids will not be covered under Medigap. […]